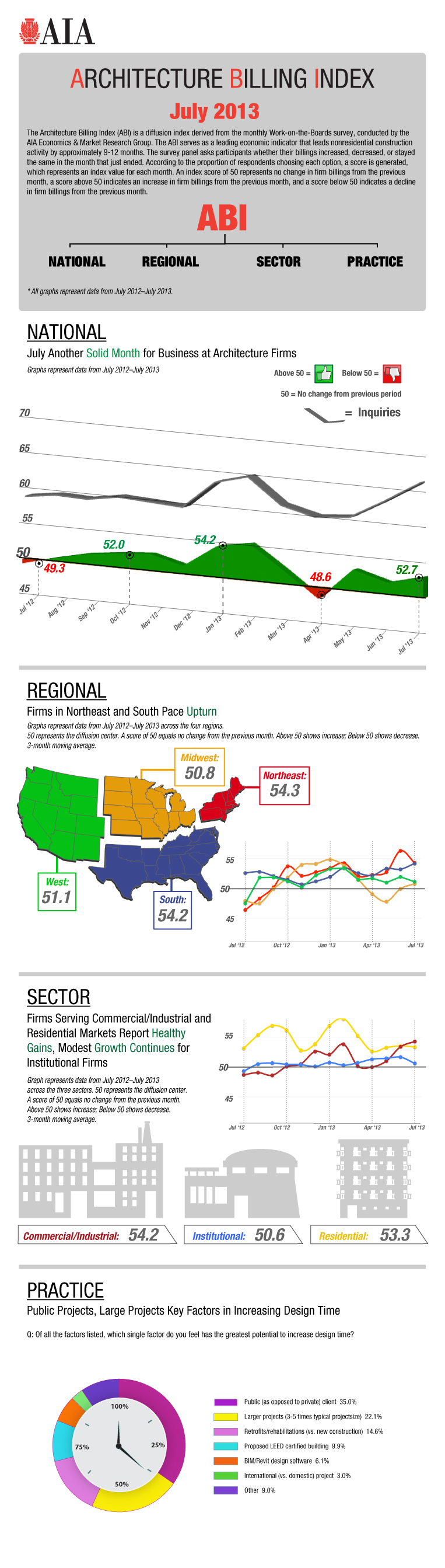

Firm Billings Up Nationwide, But Construction Sector Still Lags

Financing still cited as major reason for construction weakness

By Kermit Baker, Hon. AIA, AIA Chief Economist

Firms in all regions of the country reported billings gains in July. Firms in the Northeast and South indicated particularly strong growth, with ABI scores above 54. In the Midwest and West, firms reported more modest gains. Major construction sectors served by architecture firms also all showed gains for the month. Institutional firms, while reporting only modest gains in recent months, have now recorded 12 straight months of billings growth.

Construction not stepping up

The construction sector was expected to be one of the key engines of economic growth this year, but results to date have been disappointing. Of the more than 1.3 million payroll positions added nationally so far in 2013, the construction industry has contributed only 82,000, or just over 6 percent. Construction spending for most nonresidential building categories has declined over the past year, with some building categories, such as education and religious facilities, seeing double-digit spending declines.

Financing continues to be a major reason for the weakness in the construction sector. The second quarter survey of bank lending officers by the Federal Reserve Board reported that banks were modestly easing their lending standards for construction and land development loans. However, this modest easing has not resolved financing concerns, as these same lenders acknowledge that demand for these loans has been much stronger over the past year.

The housing market, which had finally seen rapid growth in 2012, has slowed recently. After increasing almost 30 percent last year, housing starts in July were about where they were in the fourth quarter of 2012. Single-family construction activity has been particularly disappointing. The July single-family starts figure is at its lowest level of the year, once seasonal adjustments are applied.

The uneven growth in the construction sector and in the overall economy is reflected in the volatility of consumer sentiment scores, as well as in business confidence readings. Overall business confidence as reported by the Conference Board has been generally improving over the past year. Small businesses, however, are not nearly as optimistic. Optimism scores for these businesses have not improved over the past two years, according to the business optimism index released by the National Federation of Independent Business. As a result, small businesses are not planning on adding many positions over the next three to six months.

Managing design time

As design activity has begun to recover in recent years, many architecture firms have noted that this upturn has not necessarily lead to a shorter design phase for their projects. Concern over future economic conditions, client indecisiveness, project financing problems, and difficulties obtaining regulatory approvals have all been offered by architecture firms as reason for delays in project design timelines. Additionally, though, certain project characteristics are thought to affect design time. In this month’s Work-on-the-Boards question, respondents were asked to identify project characteristics that often affect the duration of the design phase of a project. Firms identified some factors that can reduce design time. A majority of respondents felt that design/build projects reduce design time, while a significant minority of respondents felt that integrated project delivery (IPD) projects often result in a shorter design time.

However, there are many other project characteristics that tend to increase the design time of a project. While respondents had mixed opinions as to the impact of using building information modeling (BIM) on design time, the impact of other project characteristics was quite unambiguous. About 70 percent of respondents felt that retrofits to or rehabilitations of existing facilities had longer design times, as did international projects. More than 75 percent of respondents felt that larger projects, proposed LEED-rated projects, and projects with a public client typically had higher design times.

Of all project factors that could affect design time, respondents were asked to select the single factor that has the greatest potential to lengthen design schedules. Having a public client topped the list, selected by 35 percent of respondents. Coming in second were larger projects, larger defined as three-to-five times larger than the typical project at the respondent’s firm. Building retrofits and rehabilitations were selected by almost 15 percent of respondents, while about 10 percent felt that attempting a LEED certification had the greatest potential to increase design time.

This month, Work-on-the-Boards participants are saying:

- [We’re] beginning to show a slight increase in workload. [We’re] concerned about putting on additional staff and being able to maintain their employment. [We] do not like to hire and fire for workload.— 40-person firm in the South, institutional specialization

- Immensely improving. [This is] mostly related to projects that started four years ago and could not get financed since that period.—4-person firm in the West, commercial/industrial specialization

- Steady but measured improvement. Some government projects have

been delayed due to budget concerns. If they get canceled, we will start

to move backward again.—20-person firm in the Midwest, institutional

specialization

- Contractors seem to be a lot busier this summer than they have been in recent years. Bidding on projects has slowed due to workloads.—4-person firm in the Northeast, institutional specialization

No comments:

Post a Comment